FRM

국제 FRM Part 1 오답·개념 정리

khc9914

2024. 1. 4. 16:12

Chapter 1

Foundations of risk management

▶GARP Code of conduct

|

Disclosure of conflicts of interest

|

|

Follow local culture

|

|

Follow higher standard

|

|

Independence

|

|

Cannot outsource responsibilities

|

|

Clearly disclose limits of knowledge

|

|

Not overstating accuracy/certainty of result

|

▶Insurance ratio

|

Loss ratio

|

Insurance payment/Premium receipt

|

|

Expense ratio

|

Expense/Premium receipt

|

|

Combined ratio

|

(Insurance payment+Expense)/Premium receipt

|

|

Combined ratio after dividends

|

(Insurance payment+Expense+Dividend)/Premium receipt

|

|

Operating ratio

|

(Insurance payment+Expense+Dividend-Investment income)/Premium receipt

|

**생명보험업은 손해보험업에 비해 더 낮은 자본을 요구

▶Rating updates

|

Positive

|

등급 상향 가능성 多

|

|

Negative

|

등급 하향 가능성 多

|

|

Stable

|

등급 변화 없을 가능성 多

|

|

Developing

|

등급이 변할 것 같지만 방향성은 모름

|

▶IPO Methods

|

Firm commitment

|

주관사가 남은 것들 모두 인수 → Trading profit

|

|

Best efforts

|

일정 부분까지 판매 시 인수 의무 없음

|

|

Dutch option

|

높은 가격에서 시작해 점차 낮아짐

수량이 모두 떨어지면 가장 낮은 가격으로 모든 물량 판매

|

▶LTCM

High Correlation risk/High Economic leverage (Not balance sheet leverage)

▶Basel Ⅱ/Ⅲ

|

Basel Ⅱ

|

Trading/Lending 활동도 자본 적정성 평가에 포함

|

|

Basel Ⅲ

|

Systematic/Non-systematic risk 모두 고려

|

▶BA/SA Operational risk capital requirement

Business indicator

|

BIC Weight

|

Business

|

|

12%

|

Retail, Asset management

|

|

15%

|

Commercial, Agency

|

|

18%

|

IB (Corporate finance), Payment&Settlement, Trading

|

▶Data architecture

|

Semantic

|

의미론적

|

|

Conceptual

|

가장 추상적

|

|

Logical

|

Not concerned with implementation

|

|

Physical

|

구체적, Conceptual/Logical data를 Implementable data로 변환

|

▶Validation/Test set

|

Validation set

|

Two alternative models 중 더 월등한 모델 결정

|

|

Test set

|

선택된 모델의 Effectiveness 확인

|

▶Operational loss data from data vendors

Biased forward large losses and useful in determining loss severity

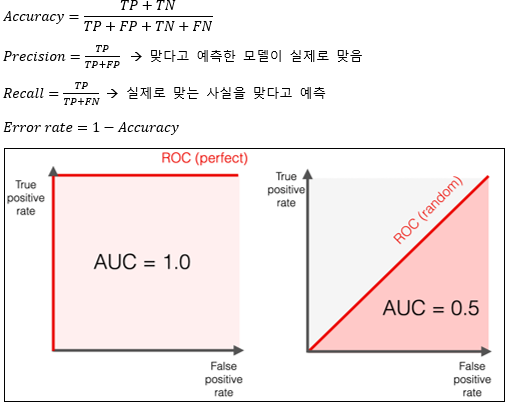

▶Confusion matrix/AUC

|

Confusion matrix

|

Model prediction

|

||

|

Positive (P)

|

Negative (N)

|

||

|

Actual

|

Positive (P)

|

TP

|

FN (TypeⅡ)

|

|

Negative (N)

|

FP (TypeⅠ)

|

TN

|

|

▶Unexpected loss risk management

Expected loss에 비해 주관성이 많이 개입되어 Risk manger의 판단이 Decision-making에 영향을 줌

▶Political risks

Democracy (민주주의): Continuous policy change, Frequent-Small changes

Autocracy/Authoritarian (독재): Discontinuous policy change, Rare-Large changes

▶RAROC

내부적 사업성 평가에 사용 (Not external comparison)

▶Risk management failures case study

|

Liquidity crisis

|

|

|

Lehman

|

단기 차입으로 비유동적 장기 자산 투자 (CDO)

|

|

Continental Illinois

|

Oil&Gas Market player, 높은 금리로 단기 자금 조달 실패

|

|

Nothern Rock

|

OTD Business Bank

|

|

Hedging crisis

|

|

|

Metallgesellschaft

|

장기공급계약 (Short)을 단기 선물 (Long)으로 롤링 헤지

마진 콜 발생 후 유동성 부족

|

|

Model risk crisis

|

|

|

Niederhoffer

|

Deep OTM Put 판매 → 극단적 상황 발생 (1일 7% 하락)

모델에서는 거의 불가능한 확률이 발생함

|

|

LTCM

|

비유동 국채 매수, 유동 국채 매도 전략 → 스프레드가 오히려 커지며 손실

|

|

London whale

|

VaR Limit을 조작

|

|

Rogue trading crisis

|

|

|

Barings Bank

|

Leeson이 회사 지시를 무시한 채 방향성 투기, 회계 조작

|

|

Reputation risk crisis

|

|

|

Volkswagen

|

테스트에서만 이산화탄소 저감 장치 장착

|

|

Governance crisis

|

|

|

Enron

|

부정 회계, 감사 실패, Not independent governance

|

|

잘못된 금융공학 상품 사용

|

|

|

Bankers Trust

|

이자율 파생 상품

|

|

Orange County

|

FRN 상품

|

|

Sachsen Landes Bank

|

Subprime 증권화 상품 투자

|

**글로벌 금융위기 이후 Fannie Mae/Freddie Mac → Nationalized, Discount window를 IB에도 개방

▶Zero-sum game

전체적으로 볼 때 위험 관리는 Risk elimination이 아닌 위험을 다른 상대로 분산시키는 Zero-sum game

▶Credit risks

|

Default risk (Insolvency)

|

Nonpayment of interest and principal → Cash-flow difficulties

|

|

Bankruptcy risk (Fail)

|

Collateral is not sufficient → Stop operating

|

|

Settlement risk

|

파생 상품 Payment risk

|

▶Risk/Reward trade-off

유동적/복잡하지 않은 상품일수록 Trade-off 관계가 분명

▶Risk Transfer/Mitigation

Transfer: 파생상품, 보험 등을 활용해 손실을 분산 (Zero-sum)

→ In practice, hedging with derivatives may not be a zero-sum game

Mitigation: 내부통제, 자산배분, 담보 확보를 통해 위험 관리

▶Risk appetite

Qualitative>Quantitative

질적 분석만으로 설정하는 경우도 존재

▶Lessons from global financial crisis

1. Need to prioritize stakeholder interests

2. Board/Risk committee should management compensation regimes

▶APT multifactor models

Flexibility, 다양한 변수들 사용 가능, 잘 분산된 포트폴리오에서 사용하기 좋음

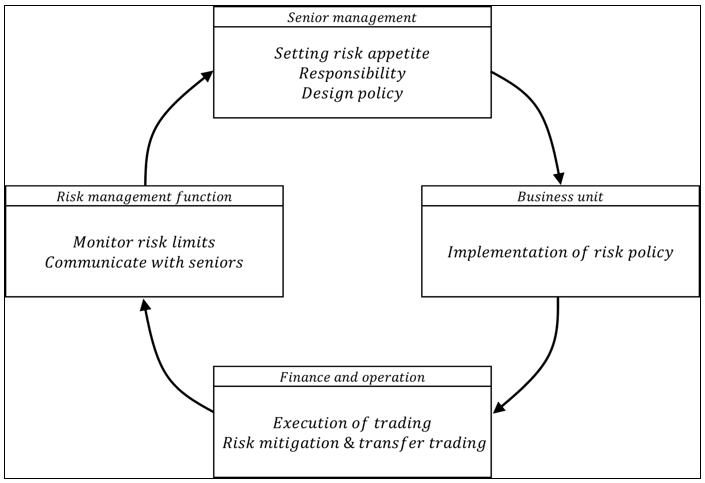

▶Silo-based vs ERM

|

Silo-based

|

Overhedging/Excessive insurance problems, Isolated, Not integrated

|

|

|

ERM

|

Target

|

Risk appetite

|

|

Structure

|

Governance (CRO, Board, Audit)

|

|

|

Identification

|

VaR, Stresstesting

|

|

|

Risks are managed within each risk units but centralized at the senior management level

|

||

▶Interdependence of functional units

▶Credit/Interest rate risk mitigation

|

Credit risk

|

Marking-to-market

|

일일정산

|

|

Exposure netting

|

파생 상품 거래 금액의 상계로 Exposure 감소

|

|

|

Loan syndication

|

여러 기관이 함께 대출을 해주어 Exposure 감소

|

|

|

Termination clause

|

사건 발생 시 계약을 종료하여 위험 상황에서의 리스크 감소

|

|

|

Interest rate risk

|

Call feature

|

Call option을 통해 이자율 변동 위험 관리

→ 이자율 하락 시 기존 채권 상환 후 더 낮은 이자율로 다시 발행

|

▶Risk advisory director

다른 산업 관련 전문가

Chapter 2

Quantitative analysis

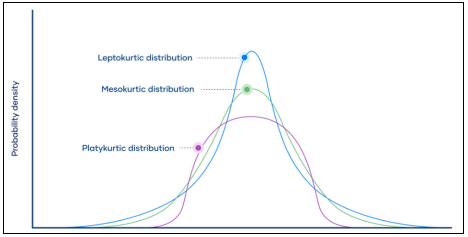

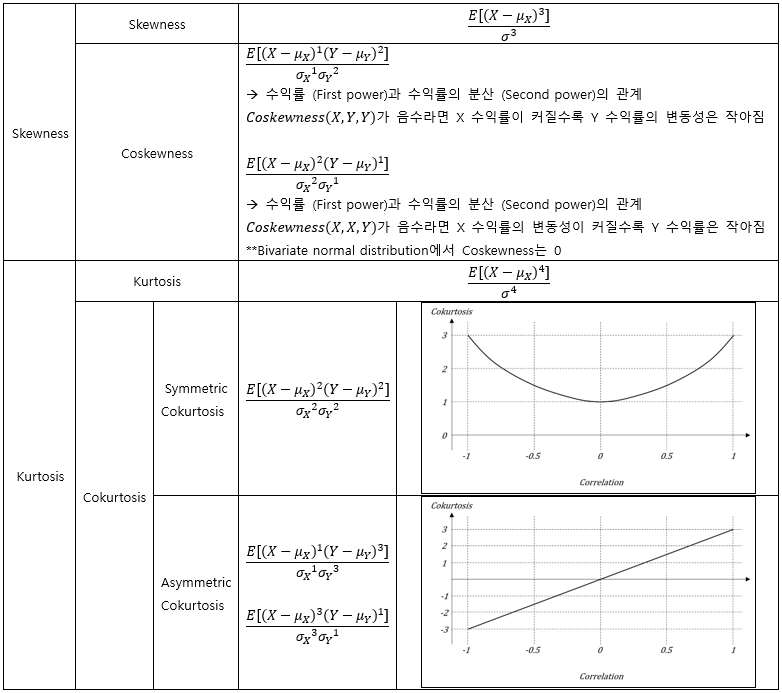

▶Skewness/Kurtosis

Positive Skewness → Mode<Median<Mean

Leptokurtic: Excess kurtosis>0 → Fatter tail

Platykurtic: Excess kurtosis<0

▶Heteroskedastic/Multicollinearity

|

Heteroskedastic

|

Multicollinearity

|

|

여전히 Unbiased/Consistency 특성 만족

하지만, OLS의 동분산 가정을 위반

|

OLS의 가정을 위반하지는 않음

|

|

Efficiency 특성 위배 → BLUE가 아니게 됨

|

Standard error가 커지는 문제점 발생

|

|

Unconditional heteroskedastic → Not major problem

Conditional heteroskedastic → Problem

|

▶White-test: Heteroskedastic 검정

▶White noise

|

Types

|

Normal distribution

|

Independency

|

|

Gaussian (Normal) white noise

|

O

|

O

|

|

Independence (Strong) white noise

|

X

|

O

|

▶Seasonality

1. Dummy variable

전체 기간보다 하나 적은 Dummy variables 추가 Ex) 분기 계절성 반영 시 3개의 Dummy 추가

2. AR/MA Model: 계절성을 반영하는 Lag variable 추가

3. ARMA Model: ACF가 점진적으로 감소하는 경우 사용 가능

▶Bootstrapping

|

특징

|

Replacement

Direct use of data (Monte-carlo simulation → Indirect use of data)

|

|

Mehods

|

1. Bagging

2. Random Forest: No replacement, Many Decision-trees

3. Boosting (Gradient/Adaptive): 이전 결과에서 틀린 것은 더 높은 가중치, 맞은 것은 더 낮은 가중치 부여

|

|

(-)

|

Hard to consider dependency (CBB로 완화)

More outliers (Fatter distribution)

|

▶Omitted variable bias

|

중요하지 않은 변수의 추가

|

Standard error 증가

여전히 Unbiased estimator 만족

|

|

중요한 변수의 누락

|

누락된 변수의 효과가 오차항에 Capture → 오차항의 독립성 위배

OLS의 본질적 문제 발생으로 회귀분석 불가능 → Biased

Correlation이 클수록 더 큰 Bias, Correlation의 +/-에 따라 Bias의 방향에 영향

|

** Omiited variable bias는 Sample size와 관계없이 발생

▶Unbiased/Biased estimator

표본평균: Unbiased estimator

표본분산: Biased estimator 하지만, n-1로 나누어주면 Unbiased 만족

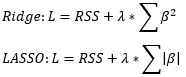

▶Ridge/LASSO//LARS

λ가 증가하면 β를 감소시키거나 (Ridge), 0으로 대체하여 (LASSO) Overfitting 방지

LARS: 모든 β를 0으로 두었다가 설명력이 높은 경우 키워나감

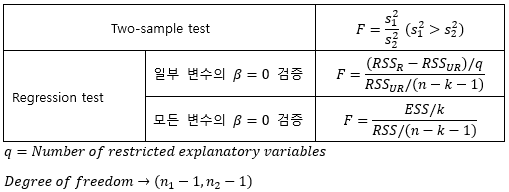

▶F-statistic

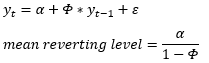

▶AR model: mean-reverting level

▶JB-test

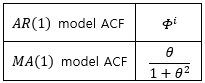

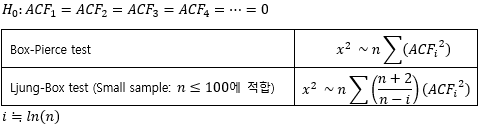

▶ACF

▶ACF test

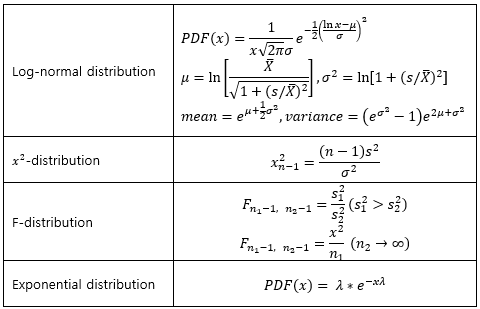

▶Log-normal distribution/x2-distribution/F-distribution/Exponential distribution

▶Penalize number of parameters

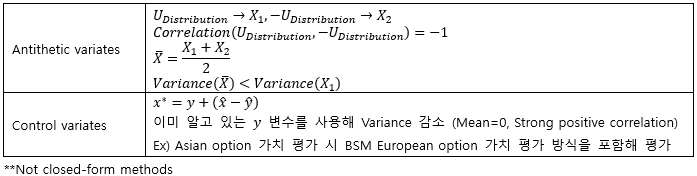

▶Monte-carlo 효율성을 높이기 위한 방법

▶Correlation types

|

Spearman correlation

|

순위의 Correlation

|

|

Kendall’s Tau

|

크기의 대소 관계가 일치하는 정도에 따라 Correlation 파악

|

**Normal distribution에서는 Rank correlation과 Pearson’s correlation이 같음

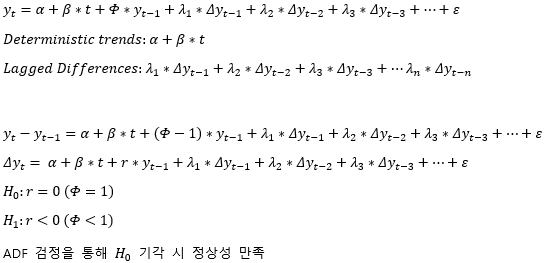

▶ADF 검정

▶Conditionally independent

서로 독립적인 사건이라도 조건부 독립은 성립될 수도 안 될 수도 있음

▶Total probability rule

Mutually exclusive: 상호 배타적 사건

Exhaustive: 사건들의 확률 합이 100%

▶Interquartile range

▶Multiple testing

유의 수준 (TypeⅠError) 증가

▶Linear transformations

▶Law of large number/Central limit theorem

|

Requirements

|

Mean finite

|

Variance finite

|

|

Law of large number

|

O

|

X

|

|

Central limit theorem

|

O

|

O

|

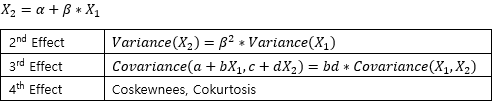

▶Cokurtosis/Coskewness

|

1차 모멘트

|

Mean

|

|

2차 모멘트

|

Covariance

|

|

3차 모멘트

|

Coskewness

|

|

4차 모멘트

|

Cokurtosis

|

▶Linear regression

Coefficients (α, β) must be linear

Not necessarily for the variables (x, y) → 비선형 데이터를 Log 등을 활용해 선형 분석 가능

▶Adjusted R2

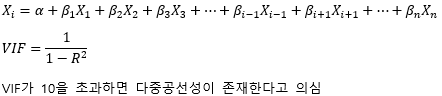

▶VIF

▶Bias-Variance trade-off

|

General-to-specific model

|

많은 변수의 모델로 시작한 뒤 가장 작은 t 통계량의 변수부터 제거해감

|

|

m-fold cross-validation

|

m-1개의 Training set, 1개의 Validation set

|

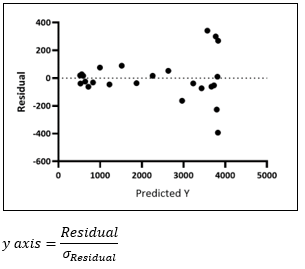

▶Residual plots

±4 Standard deviations를 넘는 경우 Problematic

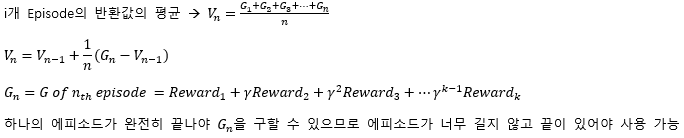

▶Reinforcement learning

학습이 증가할수록 Exploitation (아는 행동) 증가하고 Exploration (새로운 탐색) 감소

|

States

|

Environments

|

|

Actions

|

Decisions

|

|

Rewards

|

Maximize reward

|

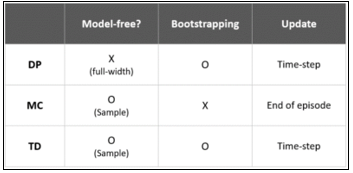

1. Monte carlo method (MC)

2. Temporal difference method (TD)

실시간으로 값을 갱신할 수 있음

▶Lag operators

AR process is covariance stationary only if its lag polynomial is invertible

▶Power law

Slow declines in tail (Fat tail modeling)

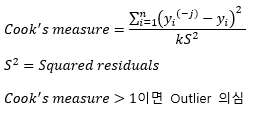

▶Identifying outliers

No outliers → 회귀분석의 Assumption 중 하나

▶NLP

|

Tokenizing

|

Identifying only the words (Only lowercase)

|

|

Remove stopwords

|

the/has/a 같은 조사들 삭제

|

|

Stemming

|

어간으로 교체 (Arguing/Argued/Argues → Argu)

|

|

Lemmatizaiton

|

단어의 기본형으로 교체 (Worse → Bad)

|

|

N-grams

|

같이 있어야 의미가 명확한 것들은 같이 둠

|

▶K-means/K-nearest neighbors

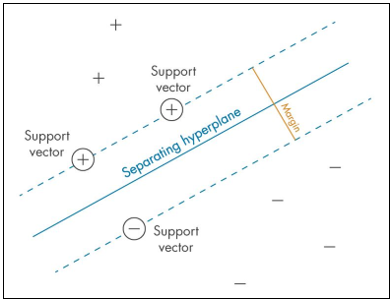

▶SVM

▶Neural networks

Find non-linear relationship

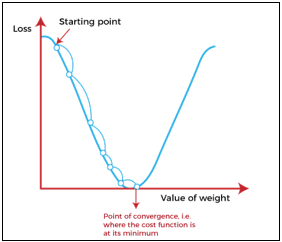

Gradient descent algorithm:

Input의 Weights를 조정해가며 Loss function이 가장 작아지는 경우를 찾음

‘기울기>0’ 인 경우 Weight를 줄이고, ‘기울기<0’ 인 경우 Weight를 늘림

Learning rate (이동간격)이 너무 클 경우 값이 수렴하지 않을 수 있으며 너무 작을 경우 Cost 多

Training set의 Loss function이 증가하더라도 Validation set에서 감소하면 → Stop gradient descent algorithm

(Overfitting 방지)

Chapter 3

Financial markets and products

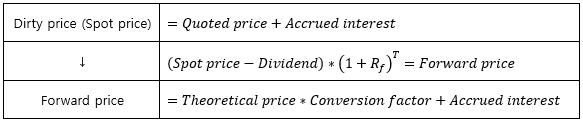

▶Interest rate swap valuation

|

액면 금액

|

$2,000,000

|

|

Fixed rate

|

7%

|

|

Payment

|

Semi-annual

|

|

Tenure

|

Spot

|

FRA

|

|

6-month LIBOR

|

6.5%

|

6.5%

|

|

12-month LIBOR

|

6.8%

|

7.1%

|

|

18-month LIBOR

|

7.5%

|

8.9%

|

Method 1

|

Tenure

|

6-month

|

12-month

|

18-month

|

|

Fixed cash flow

|

70,000

|

70,000

|

70,000+2,000,000

|

|

Floating cash flow

|

(65,000+2,000,000)

|

|

|

|

Net cash flow

|

(1,995,000)

|

70,000

|

2,070,000

|

현재 Floating-rate reset date라면 Floating-rate payments의 가치는 액면 금액과 동일

|

Tenure

|

6-month

|

12-month

|

18-month

|

|

Fixed cash flow

|

70,000

|

70,000

|

70,000+2,000,000

|

|

Floating cash flow

|

|

|

|

|

Net cash flow

|

70,000

|

70,000

|

2,070,000

|

Method 2 (FRA 적용)

|

Tenure

|

6-month

|

12-month

|

18-month

|

|

Fixed cash flow

|

70,000

|

70,000

|

70,000+2,000,000

|

|

Floating cash flow

|

(65,000)

|

(71,000)

|

(89,000+2,000,000)

|

|

Net cash flow

|

5,000

|

(1,000)

|

(19,000)

|

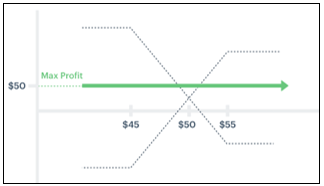

▶Box spread

Bull call spread+Bear put spread (초기에 옵션 프리미엄을 지불하고 포지션 형성)

Max profit=두 행사가의 차이

Max profit=초기 옵션 프리미엄 지불액: 무차익거래

Max profit>초기 옵션 프리미엄 지불액: Box를 Long하여 차익거래 가능

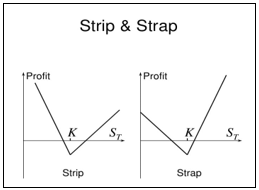

▶Strip/Strap

Strip은 Straddle에서 Put option을 하나 더 매수하여 하락에 베팅

Strap은 Straddle에서 Call option을 하나 더 매수하여 상승에 베팅

▶Delta

▶Bond returens

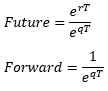

▶Eurodollar future

|

Eurodollar future

|

일일정산

기초에 이자 지급

|

|

FRA

|

마지막에만 거래

기말에 이자 지급

|

▶Bond classification

|

Clauses

|

||

|

Mortgage

|

After-acquired clause: 이미 담보된 자산을 다시 담보로 대출 불가

|

|

|

Debentures

|

무담보 대출

Negative-pledge clause: 이후 담보 채권 발행 시 해당 채권도 담보가 설정되어야 함

|

|

|

Retiring methods

|

||

|

Call

|

Fixed call: 정해진 행사가가 초기엔 높았다가 액면가로 수렴

Make-whole call: 잔존 현금흐름의 현재가치보다 높은 가격으로 행사가격 설정

|

|

|

Sinking fund

|

매년 원금 분할 회수, 담보 가치가 하락하는 경우 담보 비율 유지 가능

|

|

|

Maintenance&Replacement

|

담보 비율이 유지되도록 하는 조항

|

|

|

Tender offer (공개매수)

|

채권을 다시 사들임 (많이 사용되는 방식)

|

|

|

Start-Up company

|

||

|

Deffered-coupons

|

할인 판매, 이자를 나중에 지급

|

처음에 지급 부담이 적고

나중에 부담이 많아짐

|

|

Step-up

|

Coupon 점차 증가

|

|

|

Payment-in-kind

|

Coupon 대신 채권을 추가 지급

|

|

|

Extendable reset bonds

|

발행 이후 신용도 상승 시 금리를 낮추어 줌

|

처음에 지급 부담이 높지만 나중에 신용도 상승으로 부담이 낮아짐

|

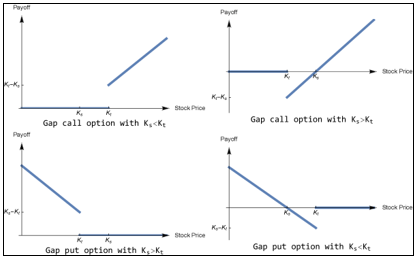

▶Exotic options

Gap option

Compound option: More Leveraged/Sensitive

▶Cheapest-to-deliver Bond

|

Upward yield curve/Interest rate>6%

|

Low-coupon, Long-maturity → CTD

|

|

Downward yield curve/Interest rate<6%

|

High-coupon, Short-maturity → CTD

|

**Wild card play: Short position 보유자가 Deliver 일자를 결정하여 Delivery cost 감소

→ Future price 감소로 Short position에게 유리

▶Swap payer/FRA long

Swap payer: Fixed payment payer, Floating payment receiver

FRA long: Floating payment receiver

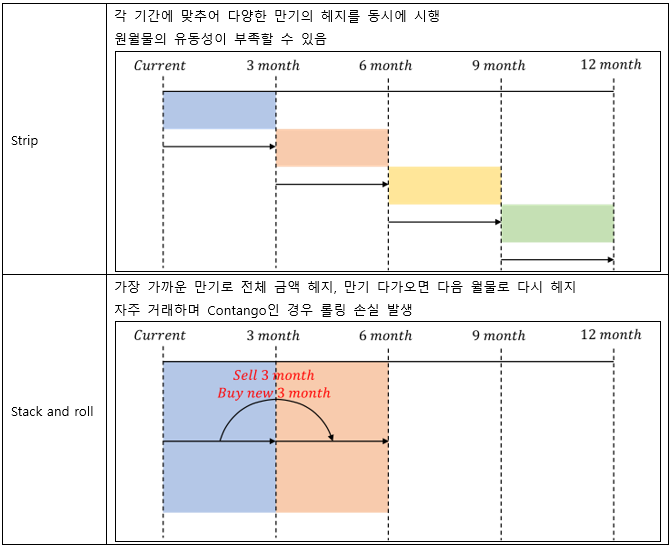

▶Strip/Stack and roll hedge

▶Increasing prepayment speed

|

Interest rate ↓

|

Prepayment speed ↑

|

|

House price ↑

|

Prepayment speed ↑

|

|

Mortgage size ↑

|

Prepayment speed ↑

|

|

만기 ↓

|

Prepayment speed ↑

|

|

Default ↑

|

Prepayment speed ↑

|

▶Zero-cost option (Zero premium)

초기에 프리미엄을 지급하지 않고 행사/만기일에 실현 손익과 프리미엄에 이자율을 적용한 금액을 함께 계산

▶Japanese bond yield

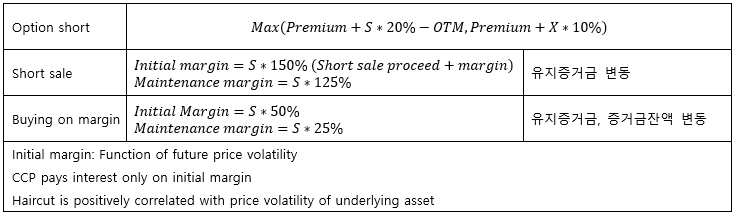

▶Margining

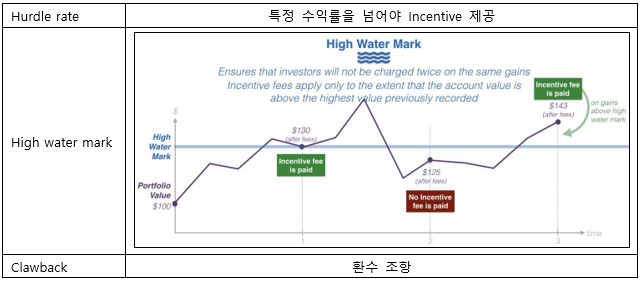

▶Hedge funds compensation clauses

▶PPP

자국 물가>외국 물가

→ 물가 차이만큼 자국 통화 가치 하락

▶Commodity future

|

Storage cost

|

농작물, 액화가스 등의 상품에서 높은 Storage cost를 보임

Metal → 보관 용이 Storage cost가 낮음

|

|

Lease rate

|

Commodity의 경우 Lease 상대의 파산으로 음수가 되는 경우도 존재

(Future price 증가)

→ 이 경우 Arbitrageurs는 Buy spot commodity, Sell future commodity를 통해 이익

|

|

Convenience yield

|

Added to lease rate

상품을 보유하며 얻는 Non-monetary benefit

|

▶Hedge accounting

1. Documented

2. 헤지 대상과 헤지 상품 간의 Reasonable한 관계

→ Hedge instrument의 이익/손실을 헤지 대상과 함께 이연하여 보고할 수 있음

▶Options

1. 주로 개별 주식 옵션은 American-style/인덱스 옵션은 European-style

2. 개별 주식/인덱스 옵션은 대부분 실물 인도가 아닌 현금 거래로만 이루어짐

▶Exotic option

1. Versatile and More efficient hedging

2. Better reflect a firm’s view on factors

3. Used for Tax/Regulatory purpose

▶FX exposure

|

Transaction

|

선물/선도환 등의 파생 상품을 통해 헤지 가능

|

|

Translation

|

해외 보유 자산의 가치 평가, Local에서의 Financing을 통해 자산을 구매하여 헤지

|

|

Economic

|

환율 변동에 의한 수요, 상품 가격 경쟁력 변화

외국에 생산 시설을 이전, 수출 통로 다변화 (가장 헤지하기 어려움)

|

▶Interest reate parity

▶DB형/DC형 연금

|

DB

|

하나의 계좌로 모아서 운용

|

|

DC

|

각 고객의 계좌로 운용

|

▶Closed/Opened funds

|

Closed

|

Opened

|

ETF

|

|

주식 수 고정

다른 투자자들과 거래

|

주식 수 유동

새로운 투자자 진입 → 주식 수 증가

투자자 유출 → 주식 수 감소

펀드 회사와 직접 거래 (장내 거래)

|

주식처럼 개장 시간에 거래 가능

다양한 거래 방식 사용 가능

(Short selling, Stop order, Limit order)

|

|

NAV가 아닌 다른 가격으로도 거래가 가능

|

매일 PM 4:00에 NAV 계산

거래 전까지 가격을 알 수 없음

(Poor price visibility)

|

|

|

Management fee (연 보수)

Sales charge (판매수수료):

Front-end, Back-end

|

||

|

Long/Short 전략 모두 사용

|

Long 전략만 가능

|

|

|

분기에 1번 보유 종목 공개

|

매일 두 번 보유 종목 공개

|

▶Day count convention

|

U.S. treasury bond

|

Actual/Actual

|

|

Money-market instruments (Treasury bills)

|

Actual/360

|

|

Corporate bond

|

30/360

|

▶Undesirable trading behaviors

|

종류

|

설명

|

불법 여부

|

|

Late trading

|

PM 4:00이후 거래

|

Illegal

|

|

Front running

|

선행 매매

|

Illegal

|

|

Market timing

|

시장가와 NAV의 괴리를 이용한 이익 추구 거래

펀드 자산의 급격한 변동이 생길 수 있어 충분한 유동성 필요

|

Not illegal

|

|

Directed brokerage

|

펀드 판매사와 펀드 회사 간의 Rebate → 시장의 신뢰 하락

|

Not illegal

|

▶Central clearing

거래 상대방 파산 시 담보물을 시가에 매각하여 Close-out하기 보단 Auction을 진행

Initial margin → 거래 상대방의 신용도가 아닌 거래의 특성, 상품 종류 등에 따라 결정됨

|

Risks

|

|

|

Default correlation is high for OTC derivatives

|

극단적 상황에서 큰 손실의 위험

|

|

OTC derivatives are priced by model

|

Model risk of pricing derivatives

|

|

Legal risk of netting (서로 다른 지역의 회사들 사이의 Netting)

|

|

|

System failure

|

|

▶Tailing the hedge

현/선물 가격 변화에 맞추어 헤지 계약 수 조정

▶Foreign currency future quote

Spot quote Bid/Ask: 1.2944/1.2952

Forward points quote Bid/Ask: 56.34/58.85 (0.0001 곱하기)

→ Forward quote Bid/Ask: 1.2944+0.005634/1.2952+0.005885 → 1.30034/1.301085

**82.4012 JPY price of CAD → 82.4012 JPY/CAD

▶LEAPS option

매년 1월이 만기인 장기 옵션

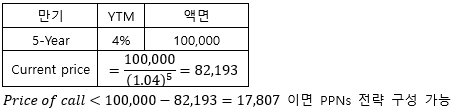

▶Principal protected notes (PPNs)

할인채와 콜 옵션을 동시에 매수해 Protective put과 비슷한 수익 구조 만듦

▶Expected return

▶Pass-through securities

▶TBA

|

Specified pools

|

Pool의 자산이 거래 전에 명확히 파악됨

|

|

TBA

|

Pool의 자산이 거래 2일 전까지 공개되지 않고 거래부터 수행

|

▶PAC and Support tranche

Support tranche가 Prepayment risk를 감수 → 그 이상의 손실은 PAC으로 넘어감 (Broken/Busted PAC)

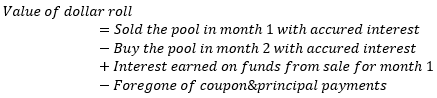

▶Dollar roll transaction

Month 1에 Pool 판매, Month 2에 Pool 구매

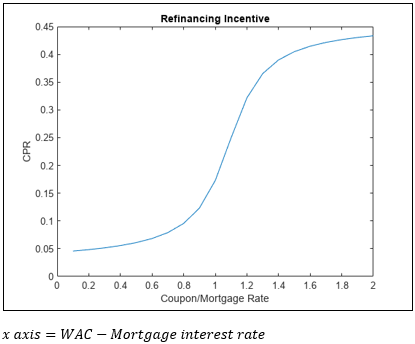

▶Incentive function of prepayments

현재 지불하는 Coupon rate (WAC)가 새로운 모기지 대출 금리보다 너무 높다고 생각되면 Refinancing 수요 증가

▶Backfill bias

Hedge fund가 성과를 보고할 때 이전의 성과들도 함께 포함됨

Chapter 4

Valuation and risk models

▶MDE(Multivariate density estimation)

|

특징

|

Non-parametric

현재와 유사한 과거 데이터에 더 큰 가중치 부여

|

|

(+)

|

현재 시장 환경 반영

Dependency 반영

|

|

(-)

|

Overfitting

많은 데이터 필요

|

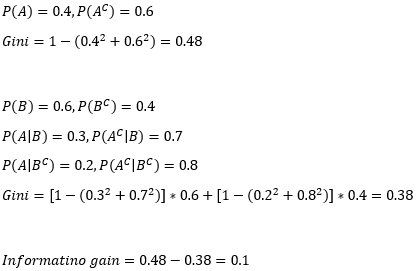

▶Gini measure: Information gain of decision tree method

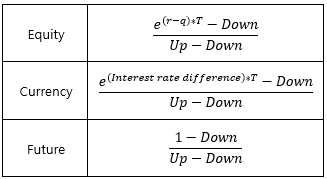

▶Binomial-Tree upward movement probability

▶Distribution of recovery rate

Bimodal (쌍봉) distribution

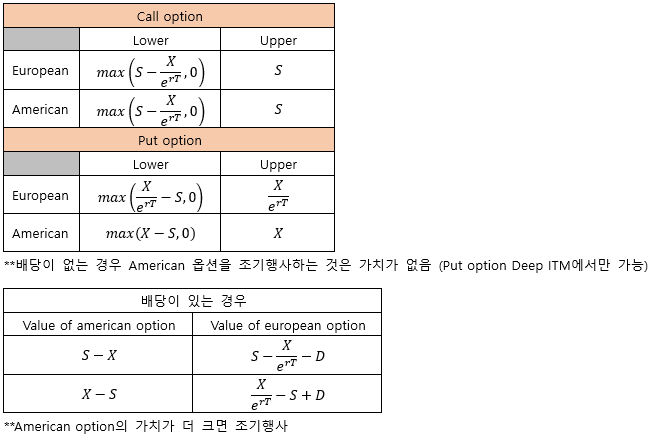

▶American/European options value

▶Forward/Spot/Par rate

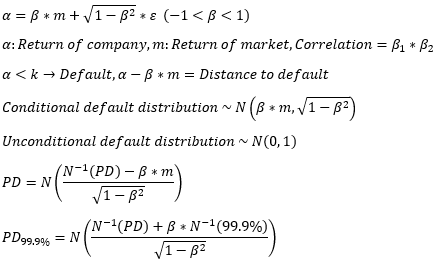

▶Vasicek model (Single-factor model)

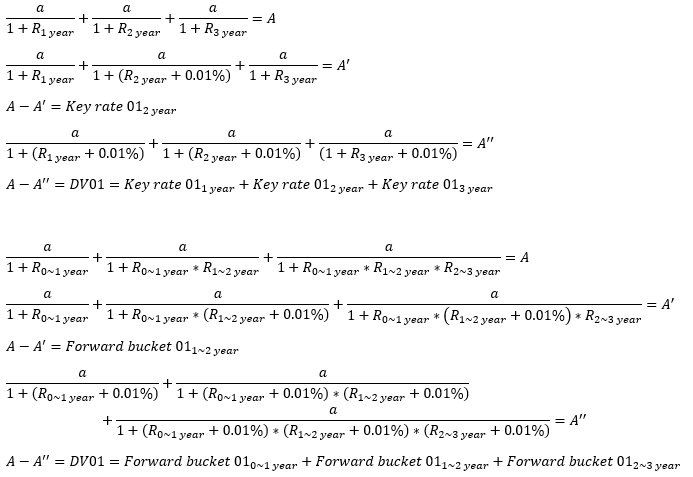

▶Key rate 01/Forward bucket 01

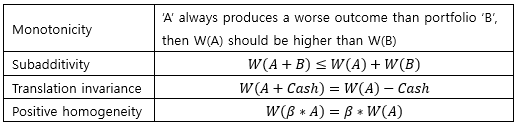

▶Coherent risk measure

▶Relation of PD and LGD

PD와 LGD는 Positive correlation

▶Impact of credit rating change

등급 상향보다 등급 하향에 더 민감하게 반응

Watchlist downgrade impact (중/단기)>Outlook downgrade impact (장기) and Actual downgrade impact

▶Stressed VaR

1. Conditional risk measure: Stress 상황에서의 데이터만 사용 → 각 은행마다 다른 기간 사용

2. Short estimation period (1~10 Days)

3. Use Historical simulation approach

▶Portfolio σ (모든 Pair가 같은 상관계수를 가진 경우)

▶Credit rating

1. Ratings for companies whose debt instruments are publicly traded

2. Periodically Reaccess

3. Rating 받는 회사가 Fee 지불 (Not investor → Conflicts of interest)

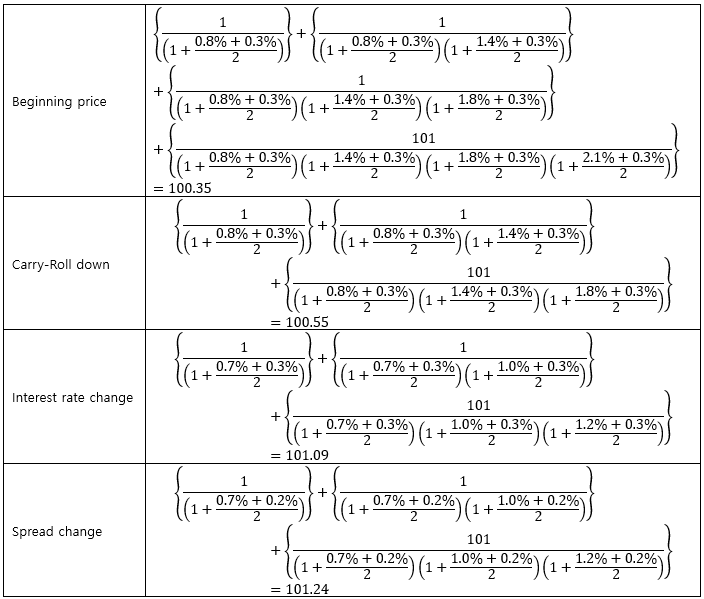

▶Component of bond’s Profit&Loss

|

Tenure

|

0.5

|

1.0

|

1.5

|

2.0

|

|

Coupon

|

1

|

1

|

1

|

101

|

|

Bond spread

|

|

|

Beginnig

|

Ending

|

|

0.3%

|

0.2%

|

|

Forward rate

|

Beginnig

|

Ending

|

|

0~0.5

|

0.8%

|

0.7%

|

|

0.5~1.0

|

1.4%

|

1.0%

|

|

1.0~1.5

|

1.8%

|

1.2%

|

|

1.5~2.0

|

2.1%

|

2.0%

|

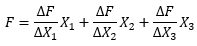

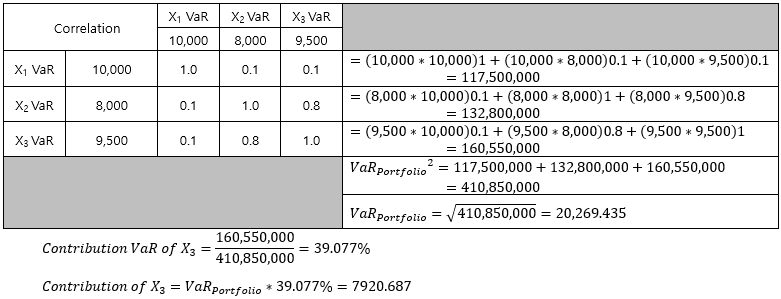

▶오일러 정리의 활용

|

Loans

|

X1

|

X2

|

X3

|

|

VaR

|

10,000

|

8,000

|

9,500

|

|

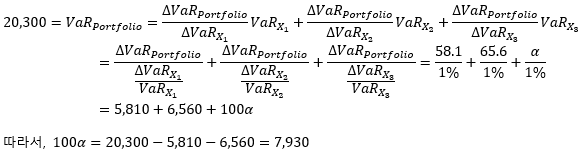

Loan VaR 1% 증가에 따른

Portfolio VaR 증가량

|

58.1

|

65.6

|

α

|

|

Correlation

|

X1

|

X2

|

X3

|

|

X1

|

1.0

|

0.1

|

0.1

|

|

X2

|

0.1

|

1.0

|

0.8

|

|

X3

|

0.1

|

0.8

|

1.0

|

**Portfolio VaR=20,300

What is the contribution of Loan X3 to the Portfolio VaR?

Method 1 (공헌 VaR 사용)

Method 2 (오일러 정리 활용)

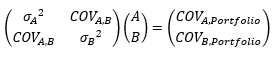

▶Covariance

▶ES

ES surface curve showing the interactions of both adjustments (Holding period/Confidence level) is convex

▶Fat-tail

Aggregation of Normal/Non-normal conditional distributions → Fat-tail Unconditional distribution

▶Actual loss/EL/UL

▶Stresstesting validation

Testing data during both stressed and non-stressed periods

▶Par rate

채권의 현재가격이 액면가와 동일해지도록 하는 Coupon rate

▶Coupon rate vs YTM

Coupon rate<YTM: 할인되어 거래

Coupon rate>YTM: 할증되어 거래

▶Barbell/Bullet strategy

|

Barbell strategy

|

High convexity, Volatile interest/Parallel increase interest rate인 경우 선호됨

|

|

Bullet strategy

|

Non-parallel changes in interest rate인 경우 Bullet 전략이 보통 Outperform

|

▶Carry-roll-down scenarios

1. Realized forward scenario

|

Period

|

Forward rate

|

Realized forward rate after 6 months

|

|

0-0.5

|

0.8%

|

|

|

0.5-1.0

|

1.0%

|

1.0%

|

|

1.0-1.5

|

1.2%

|

1.2%

|

|

1.5-2.0

|

1.4%

|

1.4%

|

2. Unchanged term structure scenario

|

Period

|

Forward rate

|

Realized forward rate after 6 months

|

|

0-0.5

|

0.8%

|

|

|

0.5-1.0

|

1.0%

|

0.8%

|

|

1.0-1.5

|

1.2%

|

1.0%

|

|

1.5-2.0

|

1.4%

|

1.2%

|

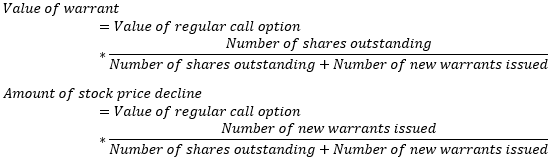

▶Warrants

▶Rho/Vega

Rho는 OTM보다 ITM에서 더 큼

잔존 만기가 클수록 Vega가 더 큼 (변동성에 영향을 받을 기간이 많음)

Vega: 변동성 1%p 변화에 따른 옵션 가격의 BP 변화

European Put ITM에서 θ>0일 수 있음

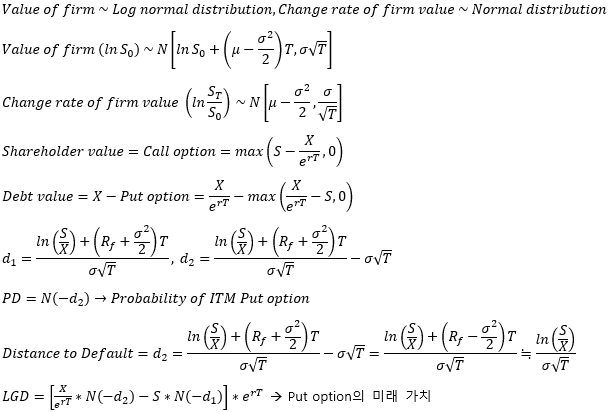

▶Merton model

**Limitations

1. 비유동적/Non-public traded asset에 사용 불가

2. 변수들이 실시간으로 변하므로 끊임없이 계산되어야 함 (계산 비용 多)

3. 관측할 수 있는 변수여야 함

4. 갑작스러운 Default 반영 불가 (Jump-to-default)

5. Investment grade bond 보다 낮은 등급의 채권 평가에 적합